FinTech Law TL;DR (June 30)

FinTech Law TL;DR (June 30)

True Lender -- Digital Wallet Complaints -- TransUnion

Hi all 👋

I’m heading to Alaska to do some backpacking for a first “post-COVID vacation,” so you may not get the next FinTech Law TL;DR for a few weeks. Try not to pass any big laws while I’m gone.

New? Subscribe to get FinTech Law TL;DR in your inbox:

House Votes to Repeal True Lender

Back in Mid-May, the Senate voted to repeal the OCC’s true lender rule. We’ve already talked about the pros and cons of the repeal (see also, this post for an explanation of what it even is).

Well, the House voted to repeal that rule this week. Their vote was unsurprising, and now the President just needs to sign the repeal, which he’s expected to do.

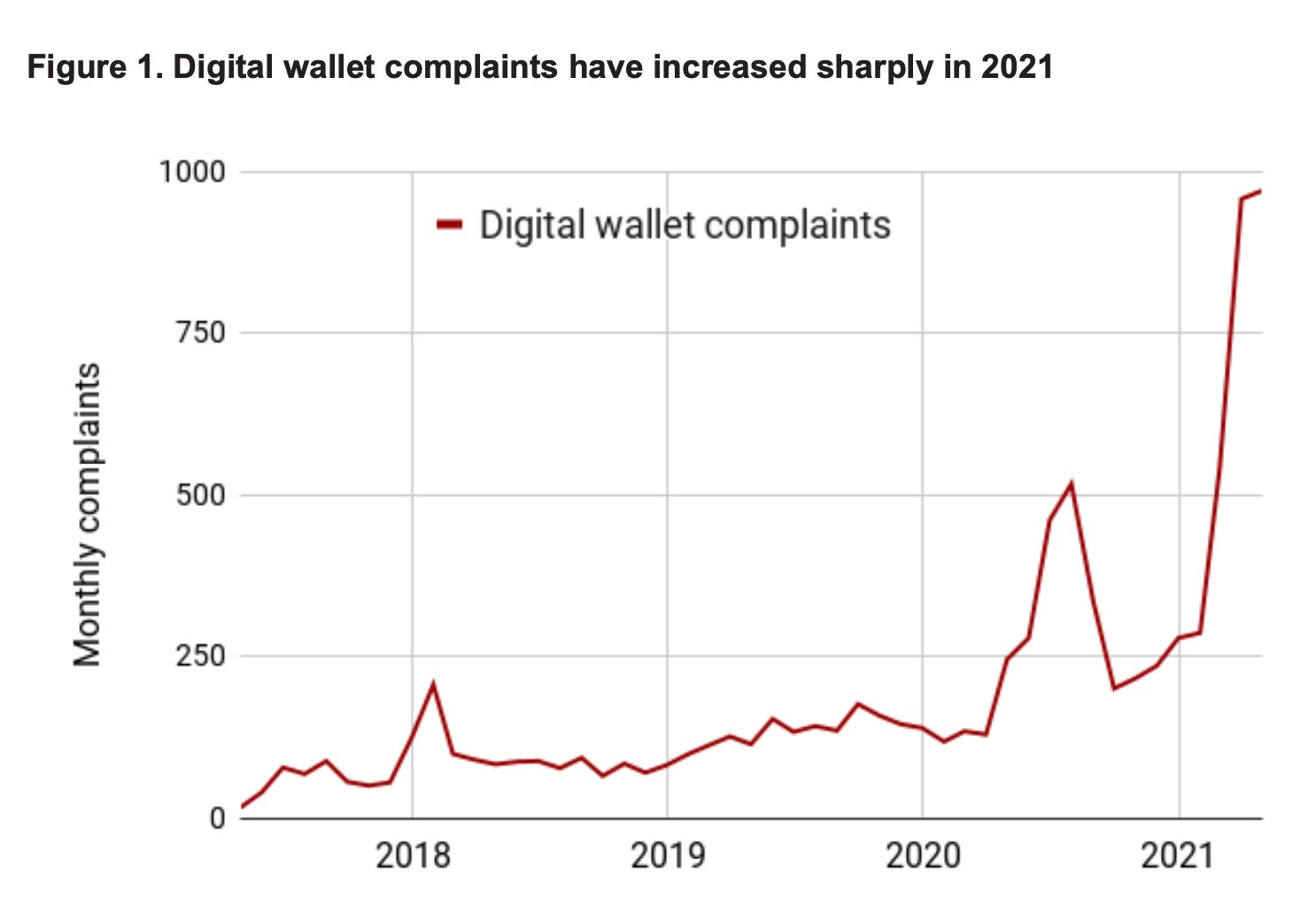

More Digital Payments? More Complaints

U.S. PIRG (a federation of US non-profits) released a report on how (1) yes, consumers are increasingly using digital payments and wallets, but (2) digital wallet complaints are on the rise:

From the graph, it’s clear complaints spiked drastically during COVID. Possibly as a result of consumers preferring contactless payment methods, and transacting more digitally during quarantines.

The report chalks the rise in complaints up to consumers being unaware they don’t have the same protections using Paypal or CashApp as they would using, say, their credit cards. And they can’t undo accidental transfers.

The most common complaints focus on:

Managing, opening, or closing accounts

Fraud or scams

Transaction issues (e.g., unauthorized transactions)

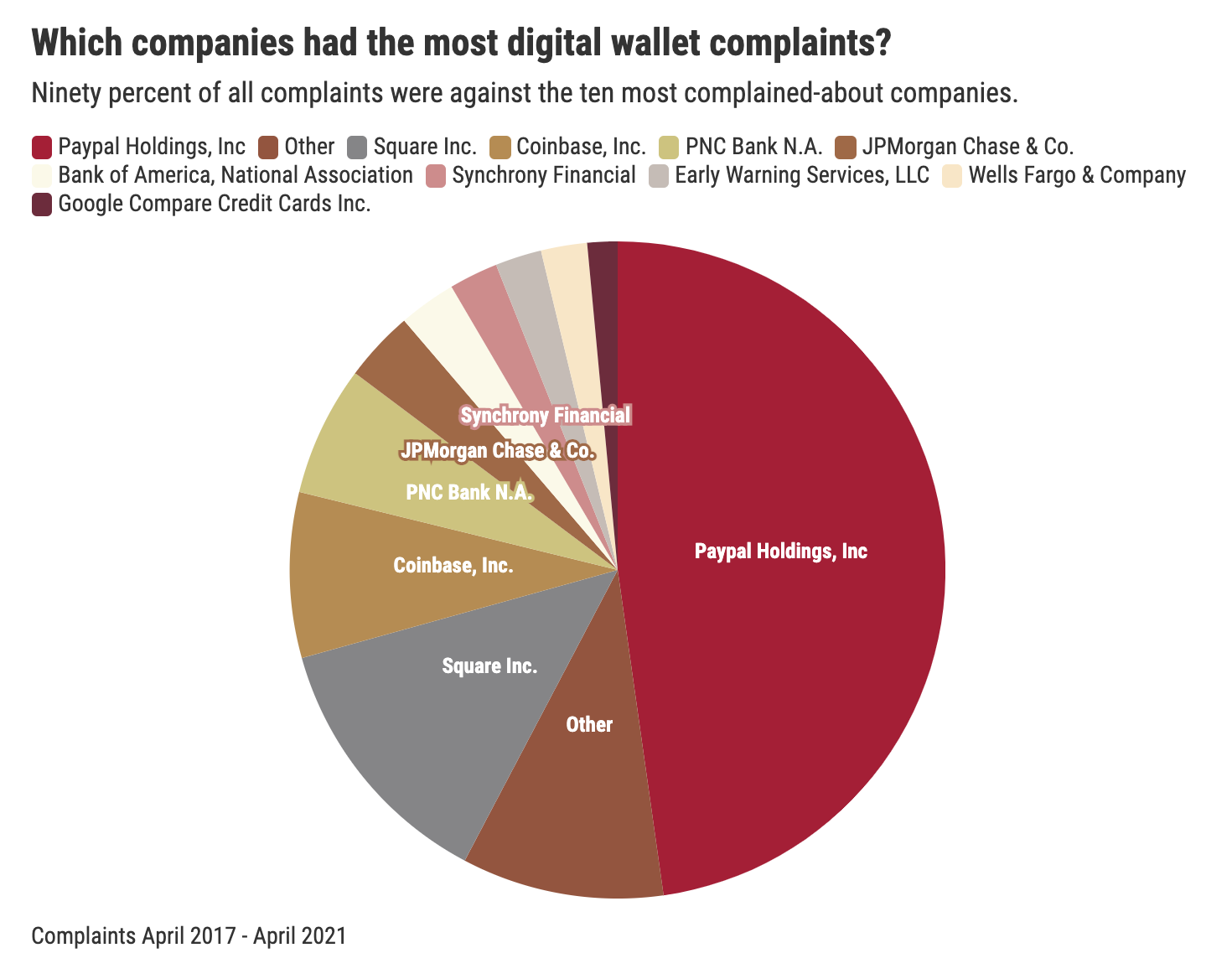

And it looks like Paypal has borne the brunt of complaints:

TransUnion Ruling

In a decision involving the Fair Credit Reporting Act (which regulates credit reporting), the Supreme Court ruled that members of a class action suit need to experience “concrete injuries.” For more details on the case, see the footnote ↗️ 1

What’s that got to do with FinTech?

The decision may make it harder for class actions against FinTech companies.

The gist of the ruling is:

Yes, the defendant technically violated a federal statute.

Yes, over 1,800 plaintiffs in the class had an inaccurate OFAC hit shown on their credit report…but over 6,300 didn’t. So the whole class of plaintiffs didn’t show there was sufficient “harm.”

So if a class action lawyer wants to bring a case, they’re now on notice they can’t just say “look, the defendant FinTech technically violated a law!” They have to show there was actual harm to the class of plaintiffs.

Is this a good thing? Maybe, maybe not.

Some class action attorneys are known for borderline extortion. But showing “concrete evidence of harm” may not be readily apparent until plaintiffs can do basic doc discovery, so they need to be able to move the case forward first.

Check out Manatt’s breakdown for more details.

Figure Charter Challenge Gets Stay

CSBS (aka, the main group of state bank regulators) received a 90-day stay on their challenge to Figure’s pending bank charter.

As a reminder, Figure’s charter is unique because it would let them make loans, handle payments, and accept uninsured deposits (over $250K). The normal bank charter trifecta includes insured deposits, so their charter app has been controversial.

Michael Hsu said the OCC is currently reviewing its bank charter framework. So it’s possible the office comes out soon and says Figure’s app is a non-starter.

This 90-day stay may also be driven by a recent decision that struck down a challenge to the OCC’s proposed FinTech charter. That was struck down because no institutions actually had applied for it so there was no harm.

Similarly here, if the OCC decides to close the door on the FinTech charter, the CSBS would be suing over nothing and incurring excessive legal costs.

2020 HMDA Data

The FFIEC released 2020 HMDA data (aka, data on house financing applications). Some interesting call outs (compared to 2019):

Refinancing of 1-4 family properties (i.e., residential property that houses 1-4 families, like a single unit house or multi-family condo) increased by 150%.

Generally, home purchase loans increased slightly for Black borrowers (+0.3%), decreased slightly for Hispanic borrowers (-0.1%) and decreased slightly for Asian borrowers (0.2%).

Non-depository mortgage lenders made up 60.7% of home purchase loans (compared to 56.4% in 2019).

See also, the Boston Fed releasing a study last week showing Black, Hispanic, and Asian borrowers were more likely to experience mortgage distress and less likely to refinance during COVID.

Elsewhere...

🖼️ Art is increasingly being scrutinized as a money laundering loophole in the US.

₿ Crypto exchange Binance was banned in the UK is pulling out of Ontario due to regulatory concerns.

⚖️ The CFPB released its highlights (lowlights?) of 2020 violations: consumer reporting agencies accepting consumer data from unreliable sources, credit redlining, mortgage foreclosure servicing violations, and student loan servicing misleading.

🏠 The Department of Housing and Urban Development released a proposal to make it easier to bring a disparate impact claim for discrimination.

₿ The IRS is asking for a $32M budget for enhancing crypto enforcement.

🏡 The CFPB released data showing there is “improving yet sustained housing insecurity risk” based on mortgage data.

📝 The FFIEC released updates to its AML/BSA Exam Manual.

📝 IL’s financial regulator released proposed regs for implementing the state’s new 36% interest rate cap law.

🤓 Dion Lisle wrote a great DeFi summary.

₿ Texas’ governor recently signed a law that modifies the state’s UCC to address crypto. Second state to do so after Wyoming.

⚖️ A Public Citizen study suggests less than 3% of fraud victims complain to a government authority.

Sui Generis

Evan Minsberg and his colleagues at Venable released a cool payments law tool kit that provides short, high-level summaries of various FinTech-related laws based on what you’re trying to do.

Marc Hauser at Reed Smith has a good, short piece pointing out what the SAFE Banking Act does and doesn’t do. It’s the main bill that protects banks from handling cannabis-related money. One notable point: it doesn’t cover non-bank lenders and non-depository, non-credit union, non-insurance company institutions.

A Baton Rouge family had $50B accidentally deposited in their bank account.

Enjoy this week’s update? Kindly subscribe (if you haven’t) and share:

About

Hi. I’m Reggie. I’m a lawyer at BlueVine. If you want to connect or are on the FinTech job hunt, come say hi on Twitter or send an email: fintechtldr@gmail.com.

Any views expressed are my own (well, sort of? I mean, they’re based on laws and regulations, so they’re not really “mine”?). Nothing here is legal or financial advice.

Here are the foundational FinTech laws and regs if you want a closer look at anything.

TransUnion placed a “potential match” alert on individuals’ accounts if their first and last name matched someone on the OFAC list (i.e., someone tagged as a potential terrorist or subject to sanctions). TransUnion didn’t provide a way for individuals to challenge inaccurate alerts. That’s all enough for a “statutory’” violation (i.e., you ran afoul of the law by reporting inaccurate info without a way to fix it). A class action was brought by over 8K individuals with those potential match alerts, claiming they were harmed under FCRA because the reports were inaccurate. But only around 1.8K of the plaintiffs had their “potential match” alert shared with third parties. As a result, they didn’t show enough “concrete injury” to get Article III standing (to sue in federal court).