FinTech Law TL;DR (Jan 24)

FinTech Law TL;DR (Jan 24)

Lithic! - Bank Charters - CBDC Paper - Credit Card Scrutiny

Hi all 👋

First, I’m super excited to say I joined Lithic last week! 🎉 If you’re not familiar, I highly recommend reading this Not Boring post on the company.

After only a week at Lithic, all I can say is…just, wow. The folks here exceed the great reputation the company already has (and we’re hiring). And if you’re interested in issuing cards to send $, spend $, sponsor your own card program, or anything else, get in touch (fintechtldr@gmail.com) and I’ll happily connect you.

Second, super super sad to be leaving the folks at BlueVine! 😥 Easily one of the hardest decisions I’ve made. All the folks at BlueVine were phenomenal, and the company has some cool stuff coming. So keep your eyes open.

Bank Charter News

SoFi, So Good

Congrats to the folks at SoFi: the Fed and OCC conditionally approved SoFi’s purchase of a small, federally-chartered community bank (Golden Pacific Bancorp).

One key feature of the approval is interesting: the new SoFi bank subsidiary cannot engage in any crypto assets or services.

The OCC is open to OCC-chartered banks doing crypto if they have sufficient controls in place. We’ve talked about their interpretive letters on here before, and some OCC chartered banks already touch crypto.

The crypto condition strikes me as a way for the OCC to say: “hey, show us you’re good enough to be a safe bank first, then we can talk about crypto.”

SoFi’s brokerage already lets customers invest in crypto, so the OCC’s probably right to call it out. The difference here is the bank will be a separate SoFi subsidiary than the one that offers crypto brokerage. So the restricted activities will be more along the lines of acting as a crypto fiduciary or holding stablecoin reserves.

I’m sure SoFi will come back asking for crypto at some point, so I’m curious to see how long the “risk on ramp to crypto” is for them, as it may be an important indicator for other FinTechs.

Regardless, it’s a promising sign for FinTechs who want to become or acquire chartered banks.

Go Figure

If you want to be a bank, you need either a national bank charter from the OCC, or a charter from the state where you’re based (e.g., Utah). For example, the SoFi-acquired bank above has a national (OCC) charter.

I like to think of banks as having three main activities that are regulated: taking deposits, making loans, and handling payments. Their charters often preempt the need for getting various, burdensome state licenses.

And, of course, a big part of taking deposits is you need to be FDIC-insured. It’s required if you’re a national bank, and practically required if you’re a state bank because state regulators almost always require it. (But there are very rare exceptions, like how the Bank of North Dakota doesn’t mention being FDIC-insured…because it’s not).

At the end of 2020, Figure (a FinTech offering mortgage, consumer loans, crypto, and other services) applied for a bank charter from the OCC. But they did something interesting and controversial: they would only accept deposits of $250K or more from accredited investors.

By limiting deposits like that, Figure believed it could avoid needing FDIC insurance. Aka, one less regulator and set of regulations to deal with. It’s an untested idea, as far as I’m aware.

Well, Figure has now amended its charter application to say nvm, we’re going to be FDIC-insured after all. We don’t know the convos that happened between the OCC and Figure…but I’m going to guess the OCC took a “hell no” stance.

Two thoughts:

We’ve talked about various FinTech bank options, but this change suggests FinTechs interested in charters should stick to traditional avenues.

The OCC’s proposed fintech charter is still out there, but it’s too risky for any company to practically spend millions pursuing. I’ve been keeping an eye on Figure’s charter + the OCC’s proposed charter because if one of them pans out, it takes away some negotiating power from bank partners and should drive down partnership costs for FinTechs. But I’m not expecting resolution on the OCC proposal any time soon.

Fed CBDC Paper

The Fed Board released a paper on central bank digital currencies (CBDCs) and opened up questions for public comment.

Let’s cover some highlights:

They define CBDC as a “digital liability of a central bank that is widely available to the general public,” “analogous to a digital form of paper money.” Aka, they’re considering non-crypto choices, though the paper mentions several crypto “experiments” and “studies” the Fed has been doing.

The paper’s model includes use of private sector intermediaries that offer wallets/accounts, since the Fed is (currently) not authorized to provide accounts for individuals.

The most interesting piece, IMO: the paper notes that a CBDC would need to protect consumers’ privacy, but also verify identities of users for KYC and anti-terrorist financing purposes. Yet it doesn’t say much about balancing those two goals. The crypto community is going to lobby hard on this point, so stay tuned.

Lastly, the Fed signaled it won’t proceed with a CBDC without the support of the President and Congress, ideally in the form of a new law.

Sidenote: the report also cites the Bank On initiative, which I heard about for the first time a few weeks ago. If you’re not familiar, it’s worth checking out. To further inclusivity, the initiative created standards for providing low-cost, low-risk consumer checking accounts.

Credit Cards Scrutiny

The CFPB released a blog post saying they’re “looking to ensure . . . robust and fair competition in the credit card market.” It has a strong antitrust vibe; “[the credit card market] is among the more consolidated markets for consumer financial products.”

The post names three focuses:

Uncover Anticompetitive Practices: The Bureau cites how major credit card players started withholding reporting credit info to the credit bureaus in 2014, which obscures some users’ behavior so it’s harder for others to offer competitive pricing.

Simplify Comparing, Switching, or Refinancing Cards: The Bureau cites how credit card ads often reference broad interest rate ranges so consumers have to have a hard credit check before they can know their actual rate, which can negatively affect credit scores and make it hard to compare cards.

I find it hard to believe this will change for the obvious reason that you can’t underwrite someone without knowing more than you normally would when you send them an ad. 🤷

Interestingly, the post cites potentially using Section 1033 (aka, the US’s “open banking” law) as a way to give consumers more power in switching cards.

Junk Fees: The Bureau cites how many credit card fees “herd” around certain levels, suggesting that competition is ineffective at driving the price down.

The Bureau doesn’t explain the logic on this one. It could be the “herding” is broadly distributed around certain levels, and competitive markets would have more starkly evident levels (because everyone is forced down to their minimum feasible fees).

We haven’t heard much from Chopra’s CFPB on credit cards until this. And the blog doesn’t mention any specific steps the Bureau will take (like launching an inquiry, or bringing lawsuits). With all the other rulemaking, drama, and competing priorities (e.g., BNPL), I’m not convinced much will come from this, but who knows.

CFPB Collector Suit

The CFPB sued a debt collection company and its owners for knowingly using third-party debt collectors that violated federal debt collection law (the FDCPA).

The compliance folks at the company objected to using the third parties after discovering violations but were ignored or overruled. Lesson: listen to your compliance team!!!

Elsewhere:

🧐 On the heels of inquiry letters to to BNPL providers, the CFPB invited the public to comment on BNPL.

⚖️ The FTC is returning more than $10M to LendingClub customers who were charged hidden fees. Most notable, IMO, is that the FTC is sending refunds via…PayPal?

✉️ The CFPB’s Acting General Counsel sent a letter to consumer advocacy groups clarifying the Bureau’s 2020 earned wage access opinion — which lays out a list of safe harbor conditions for EWA providers — does not cover instances where employees have to pay charges or tips to access the product.

🧐 The FDIC and FinCEN announced a tech sprint to help find a “scalable, cost-efficient, risk-based solution to measure” the effectiveness of methods of verifying digital identities.

👩⚖️ A DC federal district court dismissed the suit that was trying to reinstate the CFPB’s “ability to repay” payday lender rule.

🧐 Experian plans to launch a BNPL-focused bureau this year; see FinTech Business Weekly for a good breakdown of why Experian wants this approach.

🧐 The CFPB issued a bulletin saying it’ll be scrutinizing medical debt collections and credit reporting practices.

😠 JPM Chase seems to be filing lawsuits against defaulted credit card users after a CFPB consent order from 2011 expired. The expired order required JPM Chase to substantiate their suits.

📝 The FTC and DOJ kicked off a review of federal M&A guidelines by asking for public input on how to modernize them.

⚖️ Navient agreed to settle claims with 39 state attorneys general for $1.85B based on allegations it steered students into expensive forbearance options and made loans to subprime borrowers attending questionable for-profit colleges.

⚖️ A business credit report provider agreed to settle with the FTC for failing to fix credit errors and selling credit improving products that didn’t deliver.

🧐 Starting this summer, the IRS will require a selfie via ID.me to access and pay your taxes.

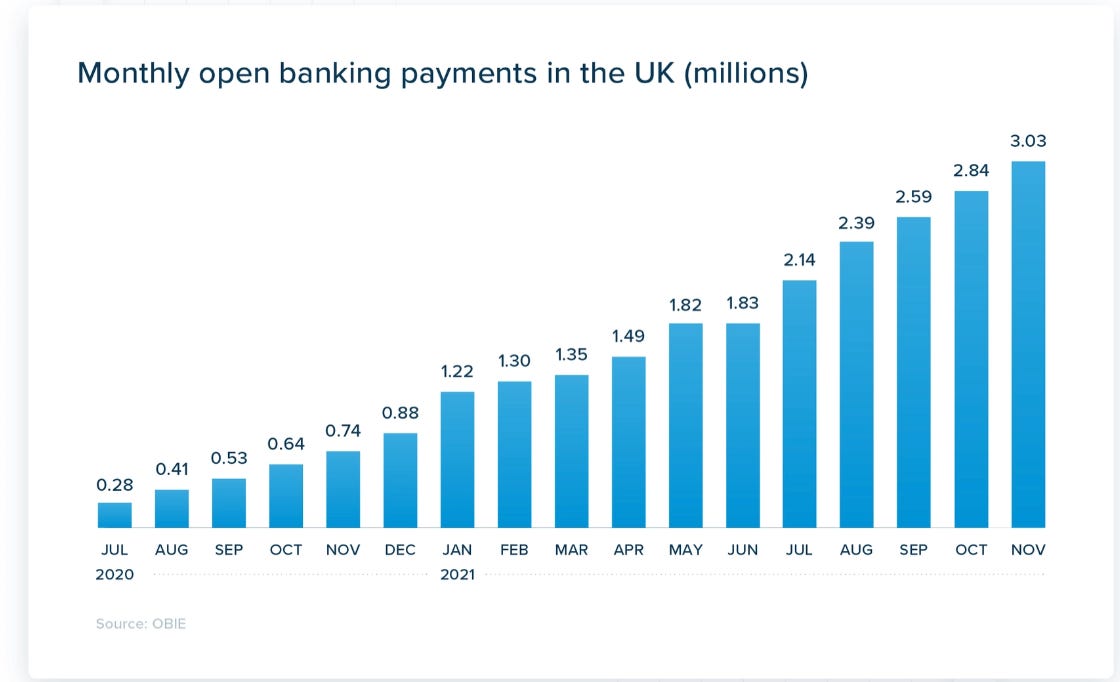

🤓Not US law-related, but here’s a really good TrueLayer piece on how the EU’s open banking law has been a success 4 years out.

Elsewhere (in crypto):

🧐 Reuters published a piece extensively laying out how Binance failed to meet money laundering regs.

📝 Head of the OCC Michael Hsu gave a speech about crypto, though it’s more of what we already know: (1) let’s apply banking regs like reserves and oversight, and (2) we need better regulatory coordination and collaboration.

💳 Mastercard and Coinbase are partnering to let customers buy NFTs with Mastercards. They’ll be classified as “digital goods” purchases (like an ebook or digital news subscription).

👎 SEC rejected two BTC spot ETF applications (NYSE Arca, and First Trust SkyBridge) because the filings didn’t meet investor protection and public interest requirements.

🧐 A consortium of US banks and others (including Figure) plans to offer their own stablecoin, USDF.

🍿 Kim Kardashian and Floyd Mayweather Jr. (among others) are being sued as part of a class action over the allegedly misleading promotion of EthereumMax tokens.

Sui Generis (Fun Finds)

The US Consumer Product Safety Commission is a real thing and whoever runs their Twitter page deserves a raise for their NFT PSAs:

My two favorite things from my angsty high school years in one, books and RATM:

About

Hi. I’m Reggie. I’m a lawyer at Lithic (we’re hiring!).

If you’re interested in issuing cards to send $, spend $, sponsor your own card program, or anything else, get in touch (fintechtldr@gmail.com) and I’ll happily connect you.

Also, if you want to chat generally, are raising pre-seed rounds, or are on the FinTech job hunt, come say hi on Twitter or send me an email (fintechtldr@gmail.com).

Any views expressed are my own (well, sort of? I mean, they’re based on laws and regulations, so they’re not really “mine”?). Nothing here is legal or financial advice.